Two weeks ago the Vietnamese government announced that their curbs on foreign ownership limits will be eased. The story has always been:

“I like the market and Vinamilk/Masan, but I cannot get my hands on any stock. All because of those stupid foreign ownership limits.”

Well – you won’t have to wait much longer. Foreign ownership limits will be raised from 49% to 100% in most major industries in September this year. It is likely to lead to massive capital inflows into the Vietnamese market.

Less strict foreign ownership limits will also enable Vietnam to be ranked by MSCI as an “emerging market” rather than a “frontier market”. There are over US$110 billion in ETFs tracking emerging market indices, and even more quasi-index funds (a.k.a. “mutual funds”) whose performance are judged against MSCI emerging market indices. They will also have to buy more Vietnamese stocks once the country has been upgraded to emerging market status.

So with a fixed supply of stocks and a massive increase in demand, only one thing can happen: stock prices will go up.

Large capital inflows will also have a second-order effect: since Vietnam is running a fixed exchange rate against the US Dollar, the State Bank of Vietnam will be forced to buy foreign currency as inflows start to pick up. An example of what George Soros would call “reflexivity”. SBV buying of foreign currency will lead to a build up of FX reserves and – unless sterilized – an increase in the narrow money supply. Inflows from 2014 has already led to an increase in m0 of +22% YoY. Vietnam’s banking system is reserve constrained and higher reserves will have a multiplier effect into broader credit growth. Some money will surely flow into the equity markets and deliver what I believe to be a solid, sustainable stock market boom.

In addition, the State Bank of Vietnam has pledged to keep monetary policy loose in 2015. The inflation rate has come down to 1% in June 2015 from 5% in June 2014, which will enable SBV to lower interest rates and still achieve its policy goal of “controlling inflation”.

Vietnam is a great country

Since the government introduced free market incentives in the economy in 1986, the economy has been the fastest growing in the world in US Dollar terms. In real terms, GDP growth has held steady at 6-8% per year.

Demographics are great: the average age is 23 years and the population grows by 1.0% per year.

Manufacturing wages are less than $2,000 per year compared with $10,000 per year across the border in China. Vietnam is following the example of China, Korea and Japan to grow its economy by infant protection and export discipline. Exports have risen 15-20% per year over the past decade and continue to grow. Samsung now manufacturers half of its mobile phones in Vietnam. In a survey in Korea, companies said that Vietnam is the most promising emerging market.

PWC expects Vietnam to be the second fastest growing economy in the world until 2050 after Nigeria.

What you see now is just the beginning.

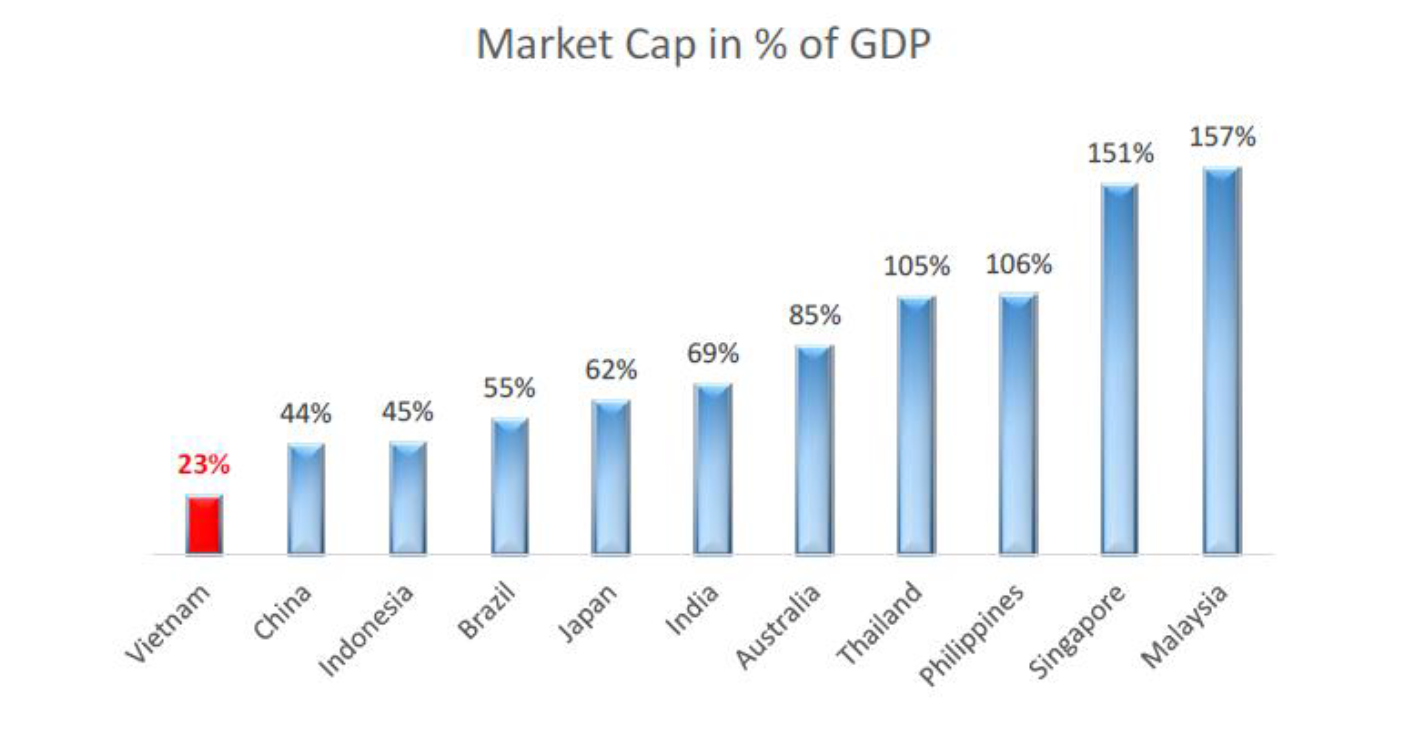

Cheap?

Market cap/GDP is among the lowest in Asia as well at 23%:

On a PE-basis, the market looks very attractive. 12x forward earnings is among the lowest in the emerging markets universe and touching its historical low as well:

If banking system profitability recovers, there is significant upside to this forward earnings estimate. A key factor in the non-performing loan issue that has plagued the banking sector is falling property prices since the 2006-2010 credit bubble.

The good news is that property prices have finally started to pick up since last year and are continuing its upward trend. Properties are cheap – consultants are quoting rental yields of 6-10% depending on the type of property. Certainly much cheaper than major cities in mainland China where yields have come down to 2-3%.

As property is often used as collateral in loan transactions, rising property prices may ease banking sector insolvency issues and boost medium-term credit growth.

So what?

Vietnam as a country is similar to China 15 years ago. Corporate governance seems to be just as bad as in China, Korea and Russia. Insider trading and front-running is rampant. A lot of the listed companies are simply rent-seeking operations that have no competitive advantage other than government protection.

So if you were a Chinese investor in the year 2000, what stocks should you have focused on? First: consumer stocks such as Moutai and Changyu and great manufacturing companies. Second: great exporters such as Gree and Haier. Third: Technology firms such as Tencent, Baidu and HIKVision. Most of these stocks have performed spectacularly, but did not offer their shares to the public until the mid-to-late-2000s.

In Vietnam, the largest consumer companies are Vietnam Dairy Corporation (“Vinamilk”), Masan and Kinh Do Corporation. Vinamilk trades at PE 14x for what is an excellent business. The future is somewhat uncertain as the current chairwoman is due to step down next year but the potential for milk consumption in Vietnam is mouth watering. Masan owns a Tungsten mine and for that reason, may not see its foreign ownership limit lifted when September comes. DHG Pharmaceutical is inexpensive and is said to be a well run firm. FPT is a technology conglomerate with a promising software outsourcing operation similar to Infosys. But management lacks focus and is reliant on its dying distribution business for much of its cash flows. Bank deposits/GDP in Vietnam is 12% vs 50% in China so the room for growth in the banking industry is massive. Then again one should be careful about banks in fixed currency regimes as they tend to lead to recurring boom/bust processes. Brokerage firm Saigon Securities is trading at a trailing PE ratio of 13x. If I am right about the coming boom in Vietnamese equities, Saigon Securities will certainly benefit – if anyone. Auto distribution is another promising industry but the companies are too small for institutional investors.

For retail investors, the only options are ETFs or mutual funds. Market Vectors Vietnam ETF is a trap though – a large percentage of the holdings is in Thailand, not Vietnam. And the stock exposure is less than exciting. Fund managers such as Dragon Capital and PXP Asset Management offer UCITS funds with OK exposure and OK fees.

Fritz

Very nice article. I’ve always been intrigued with Vietnam, but the lack of English financials has always made it difficult. Any smallcap ideas you like (say about US$100m market cap)?

LikeLike

Sorry, I forgot to reply to this comment. I don’t know Vietnamese small caps very well, but I’m happy to refer you to fund managers who specialize in them. Send me a DM on Twitter @Fritz550 and I’ll give you contact details

LikeLike